Developing and maintaining a smart contract application is difficult compared to traditional software application development and maintenance. Blockchains usually incorporate new functionality through hard forks, that typically are scheduled ahead of time to ensure that all the nodes are running the same version of the blockchain software. Due to the difficulty in upgrade, a smart contract needs to be well tested before deployment. Smart contracts run on public blockchains that have thousands of blocks created over a period of years. A smart contract may need to be backward compatible and capable of validating earlier transactions or executing other smart contracts deployed through earlier versions of the blockchain [Bosu 2019]. Steep learning curves to get familiar with a smart contract is another challenge for many developers. The codebase of a smart contract project is not only complex but also requires a sound understanding of cryptography, networking, distributed systems as well as project specific protocols. The lack of supporting tools and documentation has been a challenge for many smart contract developers. Many of the supporting tools found in traditional software application environments are yet to be developed for the blockchain context. Moreover, the tools that are currently available are seen by many developers as immature and unreliable [Bosu 2019].

To understand a complicated smart contract domain, developers are looking for good learning materials and tutorials. Even the documentation that they currently have are not user friendly. [Ayman 2019] studied smart contract related discussion on the Stack Overflow forum which caters to many types of software developers and found that questions posted related to smart contract have increased since 2015. The fraction of posts that contain smart contract questions without answers seems unusually high, and it suggests that the user base still has a lot to learn. A significant percentage of smart contract related questions have no answers at all. Very few posts on Stack Overflow discuss security-related topics in smart contracts. Many of the blockchain projects are run by open source communities. Even when functioning well, open source communities provide only limited support. Commercially supported open source communities have a base of commercial entities with business models providing long term support to those communities – but the tradeoff can be undue influence in the development roadmap. Traditional online developer forums do not seem to be generating adequate support, perhaps due to the newness of the technology.

Smart

contract platforms need [Harris 2019] to provide three properties: they need to

be deterministic, isolated, and terminable. Determinism is required so that the

distributed instances achieve the same result in their independent computations.

A smart contract can be uploaded by anyone, which introduces a risk since any

single contract may (by design or by accident) contain viruses and bugs. If the

contract is not isolated, this could impact the entire blockchain ecosystem. Termination

is required so that contracts conclude within a reasonable time and so that excess

resources are not consumed. There are at least 28 different blockchain

platforms [Yusuf 2018]. Beyond bitcoin and Ethereum, [Bartoletti 2017]

identified four blockchain platforms supporting smart contracts that had been

launched, were publicly accessible, and had a supporting community of

developers. More recently, [Rouhani 2019] identified nine blockchains as also

supporting smart contracts. The Ethereum and Bitcoin smart contracts seem to

have the bulk of the transaction volume, with the bulk of the smart contracts

on Ethereum, though statistics on private (permissioned) implementations are

often not available. Bitcoin support for smart contracts is often through the use

of side chains [Rouhani 2019]. The number and variety of platform supporting

smart contracts seems to be increasing, providing an indication of the popularity

of the approach, but also a challenge for developers and users of the technology.

Different blockchain platforms support a diverse set of programming languages to develop smart contracts. Some proposals have been made for higher level domain specific languages for smart contracts (e.g., based on specifications, or declarative logic), or to enforce solutions against particular vulnerabilities (e.g., BAMBOO – proposed to enforce a state machine model to resolve the reentrancy problem underlying the DAO hack). Languages for smart contracts should (1) consider users’ needs as a primary concern; (2) to facilitate safe development by detecting relevant classes of serious bugs at compile time; and (3) as much as possible, be blockchain-agnostic, given the wide variety of different blockchain platforms available [Coblenz 2019]. While there have been many recent proposals for language improvements, in practice, for many developers, the set of smart contract programming languages is constrained by the choice of blockchain platform.

[Bartoletti

2017] identified nine design patterns for smart contracts – token,

authorization, oracle, randomness, poll, time constraint, termination (because

the blockchain is immutable, there is a need to explicitly end a smart contact

that has completed), math, fork check, and about 80% of the smart contracts

studied used one or more of these design patterns. Validated design pattern templates

of smart contracts increase trust for counterparties. The validation removes

the need for costly back-testing and facilitates decentralized business

transactions at unprecedented scale [Kaal 2019]. [Knecht 2017] proposes a smart

contract deployment and management platform that can execute development tools

and code quality tools in a trusted way and uses this to reduce the trust

required into the smart contract developer or auditor. [Lu 2019] proposed uniform

Blockchain as a service (uBaaS) as a solution to improve the productivity of

blockchain application development. Existing BaaS deployment solutions are

mostly vendor- locked: they are either bound to a cloud provider or a

blockchain platform. In addition to deployment, design and implementation of

blockchain-based applications is a hard task requiring deep expertise. The

services in uBaaS include deployment as a service, design pattern as a service and

auxiliary services. While well-known and

time-tested design patterns can help developers, the packaging and portability

of smart contracts is still constrained by the blockchain platform selection.

Testing

blockchain software is challenging as the software executes on a distributed

and potentially hostile environment that currently cannot be adequately

simulated on a development machine. Smart contract developers typically use

‘test-nets’ to experiment with heir code before deploying it to the ‘main-net’.

The test-net simulators that smart contract

developers currently have are typically resource-limited, difficult to configure,

and are unable to completely simulate a complex and hostile real-world

environment. The scale and complexities of test-nets are typically not

representative of main-net execution environments. Formal verification

techniques have been proposed to secure smart contract projects, developers,

however, find current formal specification languages (e.g., TLA+, VDM, and

Z-notation) very complex to learn and use. Static analysis and penetration

testing tools (e.g. fuzz testing, linting …) have been useful in other

application domains for security testing, but those tools do not work well on the

smart contract code-base [Bosu 2019]. Testing frameworks, such as the truffle suite, that automatically handle

compilation and deployment of contracts and provide means of interacting with

them [Patsonakis 2019] are still evolving.

The Interactive Developer

Environments (IDEs), designed for the other application domains, seem to lack

adequate support for testing and debugging a smart contract codebase. Smart contract

developers use an array of tools for various development activities. Some

developers maintain that an IDE designed specifically for smart contract

development would help them [Bosu 2019]. Smart-contracts are typically written

using smart contract-oriented programming language such as Solidity or Vyper

and then compiled into bytecode for a specific platform (e.g., Ethereum).

Remix, a commonly used IDE for solidity, currently lacks many features such as:

error highlighting and line by line debugging, that many smart contract developers

need [Bosu 2019]. Before interacting with a smart-contract, a developer might

want to verify its security properties by decompiling its byte code but few

solutions exist for this [Bosu 2019]. The other tools requested by smart

contract developers include UML/design notations for the smart contract domain,

containers for deployment, and automated performance analysis tools [Bosu 2019].

Given the current technology maturity of many of the tools

that exist, and the variety of blockchain platforms, the environment for smart

contract development does not seem very stable. The tool chain and testing

frameworks can be expected to improve over time as developers become engaged

with the technology. For other professionals (e.g. lawyers, auditors) with

interests in verifying the correctness and completeness of smart contracts, the

situation may seem even more confusing. Progress may be more tractable by

focusing on a smaller set of well-known contracts, and establishing appropriate

processes around those first, before attempting to apply them to a broader

range of smart contracts. Focusing on particular types of tokens ay enable the

development of standardized test suites for the set of transactions supporting

those tokens. Standardized test suites would help enable the further development

of other token and transaction types.

References

[Ayman 2019] A. Ayman, et al. “Smart Contract Development

in Practice: Trends, Issues, and Discussions on Stack Overflow.” arXiv

preprint arXiv:1905.08833 (2019).

[Bartoletti 2017] M. Bartoletti & L. Pompianu.

“An empirical analysis of smart contracts: platforms, applications, and

design patterns.” International conference on financial

cryptography and data security. Springer, Cham, 2017.

[Bosu 2019] A. Bosu, et al. “Understanding the

motivations, challenges and needs of blockchain software developers: A

survey.” Empirical Software Engineering 24.4 (2019):

2636-2673.

[Coblenz 2019] M. Coblenz, et

al. “Smarter Smart Contract Development Tools.” Proceedings

of 2nd International Workshop on Emerging Trends in Software Engineering for

Blockchain (WETSEB). 2019.

[Harris 2019] C. Harris, “The Risks and Challenges

of Implementing Ethereum Smart Contracts.” Int’l Conf. on

Blockchain and Cryptocurrency (ICBC). IEEE, 2019.

[Kaal 2019] W. Kaal, “Decentralized Commerce–A

Primer on Why Decentralized Reputation Verification Systems Are

Needed.” Available at SSRN 3405401 (2019).

[Knecht 2017] M. Knecht, & B. Stiller.

“Smartdemap: A smart contract deployment and management

platform.” IFIP Int’l Conf. on Autonomous Infrastructure,

Management and Security. Springer, Cham, 2017.

[Lu 2019] Q. Lu, et al. “uBaaS: A unified

blockchain as a service platform.” Future Generation Computer

Systems (2019).

[Rouhani 2019] S. Rouhani, & R. Deters.

“Security, Performance, and Applications of Smart Contracts: A Systematic

Survey.” IEEE Access 7 (2019): 50759-50779.

There are disparate views in the literature regarding the life cycles of contracts compared with smart contracts. [Gisler 2000] identified four phases of the legal contracting process – Information (contract conception), Intention (contract preparation), agreement (contract negotiation), settlement (contract fulfillment). The smart contract life cycle in [Sillaber 2017]’s view consists of four different phases: Creation, freezing, execution, and finalization. [ISO 2019] also considered the smart contract lifecycle, but in terms of three phases: creation, operation and termination. Note that the operation phase also included consideration of modifying smart contracts in public blockchains systems, the update and rollback mechanisms supported by the blockchain and migration mechanisms defined by smart contracts. As the more recent definition, and the result of a group consensus, let us adopt the ISO life cycle structure. Gisler’s information, intention and agreement phases would map to the smart contract creation phase of ISO; the settlement phase then being the smart contract operation. Similarly, Sillaber’s creation and freezing phases map to the smart contract creation phase of ISO; the execution phase to smart contract operation; and the finalization phase to smart contract termination.

Blockchain, or, more generally, distributed

ledger, technologies are rising in popularity because of smart contracts. Not all dapps will qualify as smart contracts,

and not all smart contracts will be legally recognizable under contract law

[Guadamuz 2019] but some portion will be. A great deal of attention is given to

the practice of development, i.e. programming, of smart contracts; [AlKahlil

2019] argues that more attention should be given to the needs of lawyers as the traditional developers of contracts. Commercial

contracts are sometimes ruefully described as “documents written by lawyers,

for lawyers,” artifacts of a negotiated exchange wrapped tightly in pages of

clauses intended to insulate the agreement against litigation attacks [Barton

2019]. It is not intuitively obvious that all

of the contractual terms for some set of contracts can be implemented in

smart contract logic (i.e., many contractual terms require some aspect of

performance by external actors in the physical world); but for some subset of

contracts, smart contract can implement the necessary terms to provide value in

automating the transaction execution. In the following sections we consider

typical smart contract life cycle operations, and whether legal roles are

necessary in those phases.

The discussion is largely based on

Ethereum as the most prevalent smart contract platform. Ethereum distinguishes

between externally owned accounts (often

called users), and smart contract

accounts. For any account, its data is stored at its address. Contracts

additionally have bytecode stored at their respective addresses. This code is

executed only when receiving a call; ie the smart contract reacts as a server (in

a client server architecture) responding to requests from other clients. Transactions are signed data packages

sent from users to other users (or smart contracts); and recorded on the

blockchain. Messages are data

packages sent from smart contracts to other smart contracts or users and are

reflected in the execution trace and potential permanent data changes.

Smart contract

creation

Business lawyers add value by

structuring the agreement during its creation [Gilson 1984]. Sometimes this may

be achieved through non-price related terms such as warranties and

indemnifications [Jastrzebski 2019]. Some of these terms may be difficult to

execute directly in the smart contract, as they often rely on performance by

other actors in the physical world. For the subset of contractual terms

implementable by smart contracts, lawyers may still need to add value for their

clients by reviewing contract proposals prior to agreement and negotiating

alternative transaction structures. Negotiation on deal structuring likely

happens prior to developing the smart contract code, as any changes negotiated

would then need to be modified, essentially requiring a new smart contract to

be created. Implementation of existing

industry standardized contracts as (parametrized) smart contracts reduces the

need for contract negotiation, leaving only the contract review aspect. A

business lawyer might review a standardized contract prior to its initial use (or

upon its revision), and then develop business guidelines on acceptable

parameter ranges given other business policies, regulatory constraints etc.

Smart contract code development

typically starts with an existing contract as the objective. Code development

and testing occur prior to deployment on the blockchain. Modern software

development approaches tend to be incremental; stressing development of verifiable

functionality first with later optimization on non-functional characteristics

like performance. While devops approaches may be applicable in a blockchain

context; continuous integration/ continuous deployment (CI/CD) approaches may

be more challenging due to the nature of the blockchain. For a smart contract to exist on the blockchain,

it needs to be created by another address via the deployment (constructor) code,

which is executed once by the EVM. A smart

contract can be created by either a user or by another smart contract [DiAngelo

2019]. Contracts become deployed as part of Ethereum’s global state by wrapping

their initialization code in a transaction, signing it and broadcasting it to

the network. The state and the code of smart contracts are publicly accessible,

enabling inspections and audits [Patsonakis 2019]. Developers typically

implement their smart contracts with the Solidity language, then build the source

code using the Solidity compiler (solc) to generate the EVM bytecode. A typical

EVM bytecode is composed of three parts: creation code, runtime code and swarm

code. Swarm code is not served for execution purpose. Solc uses the metadata of

a contract, including compiler version, source code and the located block

number, to calculate the so-called Swarm

hash, which can be used to query on Swarm (a decentralized storage system)

to prove the consistency between the contract in swarm storage and the contract

being deployed. As a result, re-deploying a smart contract would result in a

different swarm code, even with the same creation code and runtime code [He

2019]. The swarm hash can provide an indication of version changes, but does

not provide indications of the scope of the change similar to other versioning

systems (e.g., semver.org)

In practice, how a lawyer could review a smart contract

implementation for these aspects is problematic unless they have also developed

skills in the appropriate smart contract platform, programming language, etc. traditional

legal skills are helpful in distinguishing subtle ambiguities in the conceptual

agreement capturing the contract, but new skills would be required to validate

the subtleties of smart contract implementations. Several implementations of distributed

ledgers have been proposed, and different languages for the development of

smart contracts have been suggested. [AlKahlil 2019] proposed a list of

requirements for a human and machine-readable contract authoring language,

friendly to lawyers, serving as a common (and a specification) language, for

programmers, and the parties to a contract.

Operational Aspects

of Smart Contracts

The costs of computing on the blockchain are non-trivial –

estimated at two orders of magnitude greater than cloud computing, and in some

cases the blockchain design requires transaction fees. Transaction fees, which

compensate miners for their work in validating transactions, are a function of

their byte size and the complexity of the code they invoke (if any). Ethereum

employs a flat cost model, i.e., each transaction byte and EVM operation costs

some predefined amount of gas. Transactions specify a gas price, which converts

ether to gas and influences the incentive of miners to include it in their next

block. The higher the gas price, the higher its real monetary cost and priority

to be mined [Patsonakis 2019]. Transaction costs provide incentives for smart

contract designers to be efficient and minimize the operational costs of their

smart contracts. There is a tradeoff

between cost efficiency for a particular smart contract vs the development and

reuse of standardized code libraries of other smart contracts on the blockchain.

Cost awareness in the code also implies a complication at code design time by

requiring this cost awareness. Cloud computing in contrast also charges for the

execution, but this decision is made at run time, and typically out of band to

the code being executed.

In light of potentially devastating financial consequences from smart contracts, several regulatory bodies have identified a need to audit smart contracts for security and correctness guarantees [Zhou 2018]. Auditors need to be able to establish the existence, valuation and ownership of assets managed by a smart contract [Pimentel 2019]. Where the blockchain is public and software inspectable, software inspecting the blockchain is limited to the digital asset; it does not reach to any underlying physical assets. Standardized tokens may facilitate such inspections, but it remains to be seen if they are sufficient for audit and other purposes. While smart contracts could be designed to monitor the results of other smart contracts for conformance to some set of rules, it is not clear that such monitoring contracts would cover the full scope of applicable compliance, financial reporting, and other regulations. In addition, common operational performance metrics like service liveness, availability etc. remain to be standardized in the context of blockchain systems (e.g. is the existence of a smart contract in the block sufficient to determine availability of the service it offers?). Lawyers may be engaged in settlement operations (e.g. a residential real estate closing), though most of the work they perform is the document review and preparation prior to the settlement meeting event. A smart contract could automate the asset transfers on a closing statement, but this still requires the prior document review and preparation by competent professionals. In the case of smart contracts, the equivalent review and preparation is likely to be focused on the creation and inspection of the securitized tokens to assure their fitness for purpose.

Mechanisms to upgrade an existing deployed smart contract are

not obvious. Barring some disruptive hard fork of the blockchain, smart

contract code is immutably recorded in the distributed ledgers. Hence, design

patterns using smart contract registries or delegatecall() constructs have

emerged to upgrade contracts; these patterns, however, introduce problems [Harz

2018]. It is difficult, but not impossible, to provide for a smart upgrade mechanism.

[McCloskey 2019] provides an example method for upgrading a smart contract

system on Ethereum.

The blockchains underlying the smart contracts also need to

be able to upgrade. Hard forks are not unknown, even in relatively mature

blockchains. In 2017 (almost 10 years after its introduction), Bitcoin upgraded

to implement “segregated witness” (“SegWit”). Some data in transactions was

moved from one portion of the block to another in a way that effectively increased

the number of transactions that could fit in each block. The blockchain before

SegWit and the blockchain after had different semantics. It takes human actions

to upgrade blockchains and Bitcoin’s users collectively acted to modify

Bitcoin’s semantics in ways that would invalidate some transactions. A critical

mass of miners announced their support for SegWit, and then on the agreed-upon

date started enforcing the new rules; everyone else went along for the ride

[Grimmelman 2019]. Governance of blockchain upgrades varies across the different

blockchain implementations. Tezos is a self-amending crypto-ledger. The

protocol that validates blocks and implements the consensus algorithm can amend

itself. Concretely a new protocol is downloaded from the network, compiled and

how-swapped to replace the current one. In order to amend itself, Tezos uses an

on-chain voting system where users of the blockchain participate to propose,

select, adopt or reject new amendments. [Allombert 2019]. Support for contract

code upgrades and explicit reference to dispute resolution procedures can be

supported in permissioned blockchains like CORDA [Brown 2016]. Blockchain hard

forks are a potentially disruptive aspect of the operational environment that should

be considered in the design of smart contracts.

Hard forks can impact the value of assets held in the distributed

ledgers, and the operation of smart contracts deployed on the blockchain. Human

action is required to implement hard forks, typically by programmers developing

the blockchain code or operating the miners. Owners of assets impacted by a blockchain

fork may seek redress from those initiating the fork [Walch 2019]. In such

cases, these developers may also need legal services. The development of

standardized behaviors for upgrades in both smart contracts and blockchains may

help reduce such liability risks during the operating phase of the smart

contract life cycle.

Termination of smart

contract

Smart contracts are supposed to be self-executing and

terminate on completion. Ethereum’s Solidity language for smart contracts

provides a function for that purpose. A Turing complete language provides no

intrinsic guarantees that a program will terminate. There are three primary

methods [Harris 2019] to guarantee termination in smart contract programs (i) Turing Incompleteness: To avoid entering

an endless loop, a Turing Incomplete blockchain (e.g. Bitcoin) will have

limited functionality and may be incapable of making jumps and loops;(ii) Steps and Fee Meters: A smart contract

can keep track of the number “steps” it has taken and then terminate once a

step count has been reached, or with a fee meter, smart contracts are executed

with a pre-paid amount put into a reserve. Every instruction execution requires

a specified fee. The contract is subsequently terminated if the fee spent

exceeds the pre-paid allocated amount; (iii) Timers: Here a pre-determined timer is maintained; if the contract

execution exceeds the time limit then it is externally aborted. Ethereum uses

the fee meter approach for termination, requiring “gas” (a fee) to deploy and

execute smart contracts. Once the gas used exceeds the pre-paid allocated

amount, the contract is terminated.

As a result of both technical and human factors, contractual

disputes can still occur, even in automated settings. Abnormal contract

terminations are typical triggers for the contracting parties to engage their

lawyers to review their options. Abnormal smart contract terminations may be due

to a mistake of fact (e.g. the smart contract reacts to reports of some

external event that are incorrect) or mistakes in operation (e.g., the smart

contract fails to terminate, or terminates early). Reliance on detecting anomalous

transactions is too late – the transaction has already been recorded on the blockchain;

and standard methods to reverse transactions on blockchains do not exist. Termination

of a legal contact and termination of a smart contract may not perfectly coincide

in time. Consider a legal contract to transfer some physical asset to a new

owner through a smart contract. The “tokenization” of the asset must occur

prior to the termination of the smart contract. The smart contract likely

concludes on the transfer of the token. The recipient may have additional steps

to gain control of the physical asset given the token representing it. Such “detokenization”

may take some time, and possibly interaction with a third party custodian of the

physical asset.

References

[AlKahlil 2019] F. Al Khalil, et al. “Trust in

smart contracts is a process, as well.” International Conference

on Financial Cryptography and Data Security. Springer, Cham, 2017.

[Allombert 2019] V. Allombert, et. al.,

“Introduction to the Tezos Blockchain.” arXiv preprint

arXiv:1909.08458 (2019).

[Barton 2019] T. Barton,

et al. “Successful Contracts: Integrating Design and

Technology.” Legal Tech, Smart Contracts and Blockchain.

Springer, Singapore, 2019. 63-91.

[Brown 2016] R. Brown, et. al., “Corda: an introduction.” R3

CEV, August 1 (2016): 15.

[DiAngelo 2019] M. Di Angelo, & G. Salzer. “Collateral

Use of Deployment Code for Smart Contracts in Ethereum.” 2019 10th

IFIP International Conference on New Technologies, Mobility and Security (NTMS).

IEEE, 2019.

[Guadamuz 2019] A. Guadamuz, “All watched over by

machines of loving grace: A critical look at smart contracts.” Computer

Law & Security Review (2019): 105338.

[Harz 2018] D. Harz, & W. Knottenbelt.

“Towards safer smart contracts: A survey of languages and verification

methods.” arXiv preprint arXiv:1809.09805 (2018).

[ISO 2019] ISO/TC307

“Blockchain and distributed ledger technologies — Overview of and interactions

between smart contracts in blockchain and distributed ledger technology systems,”

ISO/TR 23455:2019

[Jastrzebski 2019] J. Jastrzębski, “Value

Creation in Negotiations of Contractual Warranties and

Indemnifications.” European Company and Financial Law Review 16.3

(2019): 273-309.

[Rimba 2018] P. Rimba, et. al., “Quantifying the

Cost of Distrust: Comparing Blockchain and Cloud Services for Business Process

Execution.” Information Systems Frontiers (2018): 1-19.

[Sillaber 2017] C. Sillaber, & B. Waltl.

“Life cycle of smart contracts in blockchain ecosystems.” Datenschutz

und Datensicherheit-DuD 41.8 (2017): 497-500

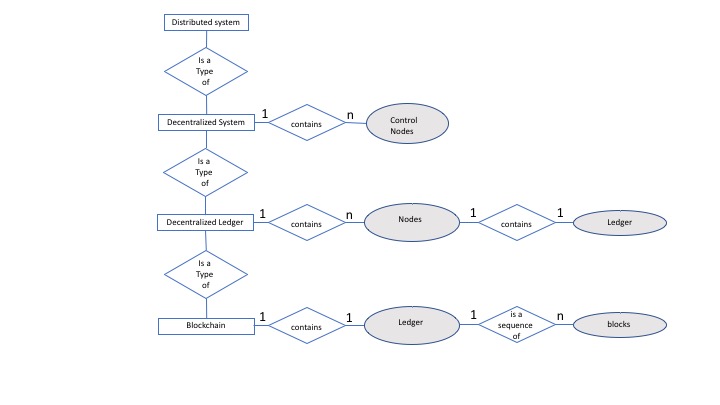

Smart contracts execute on blockchains or off-chain and store results on the blockchain. The decentralized nature of blockchains is seen by many as an important characteristic of blockchains. [Heo 2003] characterized information systems in multiple dimensions and distinguished decentralized and distributed aspects; where decentralized computing is characterized by a number of isolated processors with highly decentralized processing and low connectivity; distributed computing is characterized by a number of networked processors with highly decentralized processing and high connectivity. More recently, ISO TC 307 has been developing standards on distributed ledger technologies and offers definitions [ISO 2019] to distinguish between distributed and decentralized systems. A distributed system is a system in which components located on networked computers communicate and coordinate their actions by interacting with each other. A decentralized system is a distributed system wherein control is distributed among the persons or organizations participating in the operation of the system; Noting that in a decentralized system, the distribution of control among persons or organizations participating in the system is determined by the system’s design. A Distributed Ledger (DL) is shared across a set of nodes and synchronized between the nodes using a consensus mechanism. A DL is designed to be tamper resistant, append-only and immutable containing confirmed and validated transactions [ISO 2019]. A DL, as the name suggests, is a distributed record of transactions, maintained by consensus among a network of peer to peer nodes (possibly geographically dispersed) [Kuhn 2019]. Smart contracts, then execute in a decentralized manner on the blockchain (or DL) or record their results in the blockchain (or DL), and smart contract transactions could span multiple platforms. The Entity-Relationship diagram below should help disambiguate this terminology.

Smart contracts execute in the

context of a decentralized computing model, but the degree of distributed

control differs by the design of the underlying blockchains (primarily the consensus

mechanism). Ethereum and bitcoin have a

monolithic execution model, where all participating nodes store all the state

and execute every computation. This monolithic execution model has significant

performance impacts. One group of proposals to improve performance is sharding.

Sharding aims to split the state into shards which are distributed among

groups of nodes. Performance improves if a transaction is localized entirely

within a shard; recompilation problems can arise if the transaction is spread

across shards [Chohan 2019]. Another proposed solution is Directed Acyclic Graphs

(DAGs), which frames the ledger not as a set of blocks on a chain, but

rather as leaves out of multiple branches. A general-purpose decentralized

computing platform could be designed with a modular execution-model with secure

specialized modules, for building decentralized applications that are currently

insecure or impossible to implement with smart contracts [Alp 2019]. The

computational environment can thus be seen as a spectrum between computing

everything on all the nodes in a blockchain, computing on some of the nodes of

a blockchain (with different options on how that subset of computational nodes

are selected) , or computing offchain. Executing computational logic (e.g. the

EVM) is but one aspect of a computing model. Computation requires also storage

and communication aspects. In Ethereum the storage aspects are supported by

IPFS and Swarm. Whisper has been proposed for decentalized messaging; but has

achieved only limited support in Ethereum deployments.

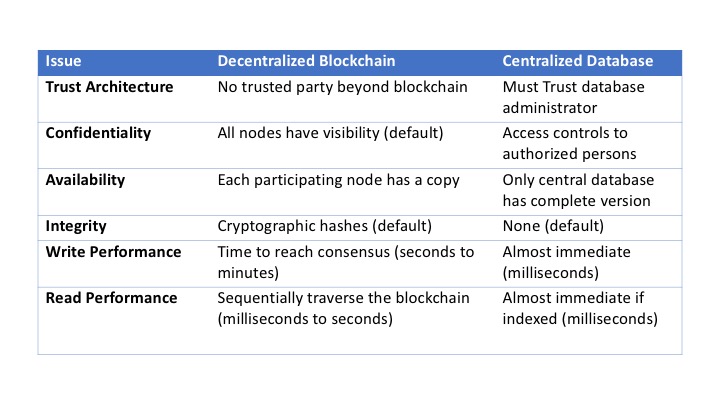

As many researchers and practitioners are discussing blockchain, some of them are raising the question about the fundamental difference between blockchain and traditional database [Chowdhury 2018]. There is a striking resemblance with the flow of a transaction in a distributed database; the major difference being the consensus protocol: databases use two-phase commit or Paxos, whereas blockchains use Byzantine tolerant protocols or variants thereof. [Dinh 2018]. The table below summarizes the differences between decentralized blockchains and centralized databases. Centralized databases have significant performance advantages and are often optimized for specific types of data (e.g., relational databases optimized for keyed data in tables ) .

From a distributed computing perspective, a smart contract resembles an object (in an object-oriented programming language). A (smart contract) object encapsulates long-lived state, a constructor to initialize that state, and one or more functions (methods) to manage that state. Smart contracts can call one another’s functions. Smart contracts are run and verified in a distributed fashion in Ethereum; the solidity smart contract semantics, however, suggest that one can think of smart contracts as of sequential programs. Smart contracts’ concurrent executions can span multiple blockchain transactions (within the same block or in multiple blocks) and thereby violate desired safety properties. Accounts using smart contracts in a blockchain are like threads using concurrent objects in shared memory [Sergey 2017]. Reentrancy and recursive calls are examples of complex behavior enabled in smart contracts (and these underlay some well-known and expensive hacks of smart contracts) where solutions exist from concurrent computing; e.g., a monitor (a well-known design pattern in concurrent programming identified in the 1970s). A monitor is an object with a built-in mutex lock, which is acquired automatically when a method is called and released when the method returns. The correctness of a monitor implementation is determined by reasoning about the monitor invariant, an assertion that holds whenever no thread is executing in the monitor. The invariant can be violated while a thread is holding the monitor lock, but it must be restored when the thread releases the lock, either by returning from a method, or by suspending via wait() [Herlihy 2019]. Concurrent programming design patterns can help make identify and resolve many of the concurrency issues with smart contracts. Smart contracts also seem to fit the object-oriented view point with tokens emerging as more specific smart contracts with some standardized behaviors.

Service Oriented Computing is another modern software

architectural paradigm where define

services are software components that can be integrated into more complex

distributed applications. Components encapsulate data to be fetched and

visualized or integrated and/or application logic to be interacted with. [Daniel

2019] distinguishes the following smart contract types: generic contracts

(implementing the application logic), libraries (stateless code meant for

reuse), data contracts providing data storage services inside the blockchain),

oracles (delivering data services from outside the blockchain). Integrating

components requires common behavior patterns e.g. push, pull, or business-protocol

based interactions. Ethereum supports transactions ( by users of the

blockchain), events (enable a contract to push information to the outside

world), calls ( messages to other contracts), and delegate calls ( invoking libraries). Data in

Ethereum transactions and events is encoded using the Application Binary

Interface (ABI), which specifies how functions are called and data are formatted.

Clients either serialize data in a binary format on their own, or by using a

suitable library function. The construct that gets closest to a description of

Ethereum smart contracts is the so-called “ABI in JSON” interface description

produced by the Solidity compiler [Daniel 2019]. Several challenges remain to fully enable

service orientation via smart contracts including search discovery and reuse,

cost awareness, performance, interoperability, standardization and composition.

A related software paradigm is microservices. Microservices are small and

autonomous services deployed independently, with a single and clearly defined

purpose. [Tonelli 2019] provides an example of implementing some functionality

as a set of smart contract microservices.

The database, object orientation, and service orientation viewpoints provide mainstream academic computer science perspectives on smart contracts; but what perspectives do practitioners actually need when developing smart contracts? [Bosu 2019] surveyed developers to capture their perspective on developing software for blockchains compared to non-blockchain environments. They noted that data stored in a blockchain is immutable (in other domains, there are several mechanisms to fix errors later by altering data); altering a blockchain ledger is almost impossible. Compared to the most non- blockchain applications that operate on centralized and/or hosted environments, dapps operate on a complex, secured, distributed and decentralized network. Blockchains use public key cryptography and cryptographic hash functions to store and verify transactions; cryptography is difficult to master and very few other domains require similar in-depth knowledge of cryptography as the blockchain domain. Moreover, knowledge of networking and networking security is required when developing for a distributed environment. The decentralized control environment also requires familiarity with consensus mechanisms, and the application itself may require domain specific knowledge (e.g. from finance industry). The developer requirement of having knowledge about diverse technological areas is a factor constraining software developers of smart contracts.

The smart contract computing context is quite complex, requiring in-depth knowledge of multiple disciplines (cryptography, networking, consensus mechanisms) and domain specific knowledge for the application. Traditional computing perspectives like databases, object orientation, concurrency, service orientation, etc., can provide some structure and alleviate some software development problems, but do not replace the need for application specific domains and in-depth blockchain implementation knowledge regarding cryptography, networking and consensus mechanisms. Much of the challenges comes from the early maturity of the implementations and the wide variety of different proposals. As the market develops, the range of practical alternative blockchains should narrow, tools improve, and the requisite body of knowledge stabilize; indeed these become prerequisites for enabling smart contracts to scale accessibility to a broader range of software developers.

References

[Alp 2019] E. Alp,

et. al., “Rethinking General-Purpose Decentralized Computing.” Proc.

of the Workshop on Hot Topics in Operating Systems. ACM, 2019.

[Bosu 2019] A. Bosu, et al., “Understanding the motivations, challenges and needs of blockchain software developers: A survey.” Empirical Software Engineering 24.4 (2019): 2636-2673.

[Chowdhury 2018] M. Chowdhury, et al.,

“Blockchain versus database: a critical analysis.” 17th Int’l

Conf. on Trust, Security and Privacy in Computing and Communications/12th Int’l

Conf. on Big Data Science and Engineering (TrustCom/BigDataSE). IEEE, 2018.

[Daniel 2019] F. Daniel, & L. Guida, “A service-oriented perspective on blockchain smart contracts.” IEEE Internet Computing 23.1 (2019): 46-53.

[Dinh 2018] T. Dinh, et al., “Untangling blockchain: A data

processing view of blockchain systems.” IEEE Trans. on Knowledge

and Data Engineering 30.7 (2018): 1366-1385.

[Heo 2003] J. Heo, & I. Han, “Performance measure of information systems (IS) in evolving computing environments: an empirical investigation.” Information & Management 40.4 (2003): 243-256.

[Herlihy 2019] M. Herlihy, “Blockchains from a

distributed computing perspective.” Commun. ACM 62.2

(2019): 78-85.

[Sergey 2017] I.Sergey, & A. Hobor. “A

concurrent perspective on smart contracts.” Int’l Conf. on

Financial Cryptography and Data Security. Springer, Cham, 2017.

[Tonelli 2019] R. Tonelli, et al., “Implementing a microservices system with blockchain smart contracts.” 2019 IEEE Int’l Workshop on Blockchain Oriented Software Engineering (IWBOSE). IEEE, 2019.

Different blockchains support

different characteristics (e.g., throughput, scalability, availability,

consistency) that may make them suitable for specific dapps. [Koens 2019] review identified 12

characteristics to compare Cross Chain Technologies (CCTs), but [Kannageisser

2020]’s review considered 43 characteristics. Blockchain design tradeoffs

limits the optimization of different blockchains ensuring that no one design

meets all characteristics at the same time. Hence more powerful dapps will need

transactions that cross blockchains. [Koens 2019] distinguishes blockchain

interoperability in the following categories: (1) Interoperability between two

smart contracts within a single blockchain (e.g. between Corda apps, which are

smart contracts on a single Corda ledger); (2) Interoperability between blockchain

platforms (e.g., between Bitcoin and Ethereum or Corda); (3) Interoperability

between a blockchain and legacy systems. (e.g., between Ethereum and a

traditional banking payment system). Cross

chain technology (CCT) helps to achieve interoperability by enabling data

exchange between blockchain designs or with external systems.

There are a number of use cases for

transactions operating between blockchains. [Buterin 2016] identified Portable

assets (tokens), Payment-versus-payment

or payment-versus-delivery, Cross-chain

oracles, Asset encumbrance and General

cross-chain contracts.

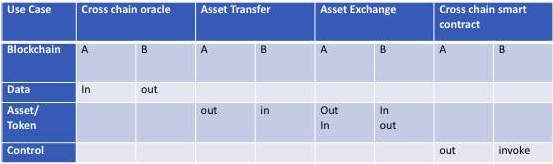

More recently [Kannengeisser 2020] identified four use cases for cross chain

technology: asset transfers, asset

exchanges, cross-chain oracles, and cross-chain smart contracts. In asset

transfers, assets are moved from one distributed ledger to another. Asset

exchanges (a special form of asset transfer), allow users to spend assets of

one blockchain in return of assets from another distributed ledger (e.g.,

trading of cryptocurrencies or other assets). Rather than moving assets,

cross-chain oracles, in contrast, provide information from one distributed

ledger to another. Cross-chain smart contracts describe the ability to trigger

the execution of a smart contract on another distributed ledger, which can

increase the level of automation. The literature identifies other use cases,

but [Kannengeisser 2016] argues these are combinations of the previously

presented use cases (e.g., sharding can be assigned to the cross-chain oracle

use case). The table below summarizes

these use cases. Assets are distinguished

from other data because they represent some notion of value e.g. a token. Asset transfers and exchanges may imply some

notion of token portability as desirable- recall that tokens have some common behaviors

not just a data type, and token portability would require those behaviors to be

executable in the context of both blockchains.

[Buterin 2016] Identifies three main design patterns for blockchain interoperation: notary

schemes, where a (trusted) party

or a group of parties agree to carry out an action on chain B when some event

on chain A takes place; Sidechains/relays, systems inside of one blockchain

that can validate and read events and/or state in other blockchains); Hash-locking (setting up operations on chain A and

chain B that have the same trigger, usually the revelation of the preimage of a

particular hash). [ISO 2019] provides some consideration of information

transfer between blockchains, but only considers cross chain and side chain

transactions. [Kannegeisser 2020]’s structured review identified three distinct

patterns: manual asset exchange (MAE), notary schemes, and relays,

as well as a fourth, hybrid pattern, which includes the three distinct

patterns. [Kannegeisser 2020] considered hash locking to be applicable in all

of the identified patterns.

Blockchains have been around for

about 10 years, but it has been the emphasis on smart contracts over the last 5

years that has raised increased the interest in alternative crosschain

arrangements to support a broader range of applications beyond cryptocurrency

trading. In this environment, the academic literature is reacting to new

commercial and open source development activities and trying to balance that

with more traditional academic studies. [Koens], for example, discusses the

cosmos and polkadot interoperability solutions that they felt were commonly

deployed. [Kannengeisser 2020] focused more on published literature but in a

structured review process its not easy to capture information sources not in

academic literature. Despite the

importance of CCTs to a number of proposed applications for smart contracts,

they remain a potential weak spot in the trust chain and may have other

performance issues. Consensus protocols on one blockchain already limit

computational throughput for smart contracts.

Transactions requiring consensus across multiple blockchains will likely suffer further performance degradations. From the perspective of blockchain as a database, transactions on that database should be “atomic” i.e., they either completely succeed or roll back to the prior state with no change made. For transactions across blockchains the mechanisms of both blockchains assuring atomicity have to be satisfied (see e.g., [Herlihy 2018]). While traditional databases commonly provide mechanisms for atomicity, the distributed nature of blockchains also creates other challenges for transactions around determinism and idempotency (see e.g., [Demir 2019]. Single point interconnection mechanisms avoid these issues, created others as the single points must be trusted and may be susceptible to failure. Blockchain consensus mechanism are deterministic in the sense that honest nodes achieve the same results from all nodes, but if the distributed nodes obtain inconsistent off-chain data (e.g., due to a time varying source read at different times) this inconsistent data can cause the consensus mechanism to fail because all the honest nodes will no longer reach the same result. Transactions are idempotent if repeatedly invoking the same transaction does not change the result. With the distributed nodes of a blockchain all generating output transactions to impact external systems, those external systems need to react in an idempotent manner to avoid inadvertently repeating a transaction. Note that this applies to external systems that are not blockchains as well. This may be problematic for legacy systems that were not designed to accommodate multiple attempts to invoke the same transaction. This is also problematic for cross-chain smart contracts that invoke control of cyber-physical systems where a single controller paradigm is common. This is not to suggest that such problems are insoluble, but rather there is some tradeoff in computing resources required (e.g., additional state, communication etc.), and the design patterns for such solutions may not be ones that many software developers are familiar with.

[Demir 2019] M. Demir, et al. “Security Smells in

Smart Contracts.” 19th Int’l Conf. on Software Quality,

Reliability and Security Companion (QRS-C). IEEE, 2019.

[Herlihy 2018] M. Herlihy,”Atomic cross-chain

swaps.” Proceedings of the 2018 ACM Symposium on Principles of

Distributed Computing. ACM, 2018.

[ISO 2019] ISO/TR 23455:2019(en), “Blockchain and

distributed ledger technologies — Overview of and interactions between smart

contracts in blockchain and distributed ledger technology systems”

Buterin’s white paper [Buterin

2014] described smart contracts as “systems

which automatically move digital assets according to arbitrary pre-specified

rules”. [ISO 2019] defined an “asset” anything that has value to a

stakeholder and a “digital asset” as

one that that exists only in digital form or which is the digital

representation of another asset. Similarly, a “Token” digital asset as representing a collection of entitlements.

The tokenization of assets refers to the process of issuing a blockchain token

(specifically, a security token) that digitally represents a real tradable

asset—in many ways similar to the traditional process of securitization

[Deloitte 2018]. A security token could thus represent an ownership share in a

company, real estate, or other financial asset. These security tokens can then

be traded on a secondary market. A security token is also capable of having the

token-holder’s rights embedded directly onto the token, and immutably recorded

on blockchain.

Recall that smart contracts started

as an enhancement providing a programmable virtual machine in the context of

blockchains, and the initial applications of blockchains were cryptocurrencies.

Cryptocurrencies have been recognized as commodities for the purpose of

regulations on derivatives like options and futures. High-value smart contracts

on cryptocurrency derivatives require substantial legal protection and often

utilize standardized legal documentation provided by the International Swaps and

Derivatives Association (ISDA). Smart contracts managing cryptocurrency derivatives

aim to automate many aspects of the provisions of the ISDA legal documentation

[Clack 2019]. There have been a number of efforts to extend blockchains and

smart contracts beyond cryptocurrency applications to manage other types of

assets. Initially these were custom dApps, but as interest in smart contracts

for specific types of assets grew, then a corresponding interest developed in

having common token representations for particular types of asset, enabling

broader interoperability, and reducing custom legal and development risks and

costs. Rather than having specialized blockchains for supply chain provenance

and other for smart derivatives contracts, different tokens representing those

asset classes can be managed by a smart contract independently of the

underlying blockchain technology.

Not all tokens are intrinsically

valuable, many derive their value by reference from some underlying asset. [Bartoletti

2017] classifies smart contracts by application domain as financial, notary

(leveraging the immutability of the blockchain to memorialize some data), games

(of skill or chance), wallet (managing accounts, sometimes with multiple

owners), library (for general purpose operations e.g. math and string

transformations) and unclassified (The financial and notary categories had the

most contracts.). The notary smart contracts enabled the smart contracts to

manage non cryptocurrency assets. [Alharby 2018] classified smart contract

literature using a keyword technique into: security, privacy, software

engineering, application (e.g. IoT), performance & scalability and other

smart contract related topics. The

application domains were identified as: Internet of Thing (IoT), cloud computing,

financial, data (e.g., data sharing, data management, data indexing, data

integrity check, data provenance), healthcare, access control &

authentication and other applications. [Rouhani 2019] categorized decentralized

applications in seven main groups include healthcare, IoT, identity management,

record keeping, supply chain, BPM, and voting. However, the blockchain-based

applications are not limited to these groups. Keywords and application

identification, provide a view of the breadth of applications, but these are

not exclusive or finite categories – new applications or keywords can always be developed extending those

lists. Token based music platforms have been proposed [Mouloud

2019]. Networked digital sharing economy services enable

the effective and efficient sharing of vehicles, housing, and everyday objects

utilizes a blockchain ledger and smart contracting technologies to improve peer

trust and limit the number of required intermediaries, respectively [Fedosov

2018]. The tokenization of sustainable infrastructure can address some of the

fundamental challenges in the financing of the asset class, such as lack of

liquidity, high transactions costs and limited transparency [Uzoski 2019].

Tokens can also be useful from a privacy perspective. Tokenization, the process

of converting a piece of data into a random string of characters known as a

token, can be used to protect sensitive data by substituting non-sensitive

data. The token serves merely as a reference to the original data; but does not

determine those original data values. The advantage of tokens, from a privacy

perspective, is that there is no mathematical relationship to the real data

that they represent. The real data values cannot be obtained through reversal [Morrow

2019]. If the costs of tokenizing and marketing new asset classes are

lower than costs of traditional securities offerings, then this can enable

securitization of new asset classes. The ability to subdivide the some types of

tokens may enable wider markets through reduced minimum bid sizes.

In 2004, early proposals were made for

XML data type definitions to capture electronic contracts [Krishna 2004]. In

2015, the Ethereum developer community adopted ERC-20 (which specifies a common

interface for fungible tokens that are divisible and not distinguishable) to

ensure interoperability [Vogelsteller 2015]. While the initial token

applications may have been for cryptocurrencies, blockchains (especially

ethereum) are being applied in a lot of other domains, and so assets administered

by the smart contracts are being stretched beyond their original purpose to

enable new applications. Studies of trading patterns would need to distinguish

whether those tokens were all being used to represent the same kind of asset to

be able to make valid inferences about a particular market for that asset.

Stretching beyond the fungible cryptocurrencies to enable popular new

blockchain applications like tracking supply chain provenance requires a a

different kind to token, a non-fungible token. Non-fungible tokens (NFTs) are a new type of unique and indivisible

blockchain-based tokens introduced in late 2017 [Regner 2019]. The

Ethereum community in 2018 adopted ERC-721 which extends the common interface

for tokens by additional functions to ensure that tokens based on it are

distinctly non-fungible and thus unique. [Entriken 2018].

In 2018, [FINMA 2018] identified 3 classes of tokens – payment tokens,

asset tokens and utility tokens. A utility token as intended to

provide access digitally to an application or service, by means of a

blockchain-based infrastructure. This may include the ability to exchange the

token for the service.

Token functions –

payment

{Utility, asset, yield}

Token features –

stake rewards

sole medium of

exchange

Token distribution

–

Initial drops and

reservations for miners and service providers

In 2019, [Hong 2019] proposed a

non-fungible token structure for use in hyperledger, and [Cai 2019] proposed

universal token structure for use in token based blockchain technology. Also in

2019, an industry group, the Token

Taxonomy Initiative, proposed a Token Taxonomy Framework [TTI 2019] in an

effort to model existing and define new business models based on it. TTI

defines a token as a representation of

some shared value that is either intrinsically digital or a digital receipt or

title for some material item or property and distinguishes that from a

wallet which is a repository of tokens attributed to an owner in one or more

accounts. TTI classifies tokens based on five characteristics they possess: token type (fungible or not), token unit (fractional, whole,

singleton), value type (intrinsic or

reference), representation type

(common or unique), and template type

(Single or hybrid). The base token types are augmented with behaviors and

properties captured in a syntax (the token formula). Particular token formulae

would be suitable for different business model applications – e.g. loyalty

tokens, supply chain SKU tokens, securitized real property tokens, etc. This

Token Taxonomy Framework subsumes the functions, features and distribution

aspects of the FINMA token model, enabling those regulatory perspectives as

well as other properties of particular value in enabling different token-based

business models.

The immutable, public Ethereum

blockchain enables study of the trading patterns in ERC-20 tokens, revealing

trading networks that display strong power-law properties (coinciding with

current network theory expectations) [Soumin 2018]. Even though the entire

network of token transfers has been claimed to follow a power-law in its degree

distribution, many individual token networks do not: they are frequently

dominated by a single hub and spoke pattern. When considering initial token

recipients and path distances to exchanges, a large part of the activity is

directed towards these central instances, but many owners never transfer their

tokens at all [Victor 2019]. There

is strong evidence of a positive relationship between the price of ether and

price of the blockchain tokens. Token function does impact token price,

over a time period that spans both boom and bust. The designed connection can

be effective; linking a project that has a value, with a token that has a price,

specifically in the absence of a legal connection or claim [Lo 2019]. From

these preliminary studies, tokens seem to exhibit some of the trading

properties of regular securities. Many of these initial tokens have no or

untested legal connections to the underlying assets. While consistent behavior

in boom and bust is important for an investment, from a legal perspective, the

predictability of outcomes for asset recovery during more stressful events

(e.g. bankruptcy) may be more important.

A point of concern is understanding

how tokens representing value will remain linked to the real asset that they

represent. For example, imagine if you own tokens representing a small fraction

of a set of gold coins at a bank, and some coins are stolen. Or the reverse –

who owns the gold coins if the account keys are lost or the token destroyed? Being

able to rationally predict what happens to your token and to the other token

owners is crucially important, since the value of tokens becomes greatly

undermined if they cannot be proven to be linked to real-world assets [Deloitte

2018]. In these types of cases, off chain enforcement action is required. A

typical legal tool for representing such interests in real assets would be recording

security interests and liens in real property under the UCC. One approach would be to update the lien

recordings for the new owner after each transaction. There are at least two

difficulties with this approach. First, the smart contract of today may not be

able to interact with manual off-chain legal recordation processes for security

interests. Secondly, if the purpose of tokenizing the asset was to increase

liquidity, frequent transactions may result in a high volume of updates

overloading off-chain manual recordation processes. Another approach would be

to use some centralized custody agent (similar to physical custody) and have

them hold the lien in the public records as a trustee (perhaps keeping account

records reflecting updates from transactions on a blockchain). If the smart

contract was a legal entity (e.g., a Vermont style BBLLC), then the BBLLC could

be the entity with the security interest in the public records directly.

However – the smart contract would need to be able to respond to legal actions

on the lien; and may incur other obligations when acting as the custodian

(e.g., reporting, insurance, licenses, etc.). The asset custodian as a

traditional entity vs the BBLLC dApp provides alternatives for consideration.

Traditional asset custodians provide an identifiable party from whom

reparations can be sought in the event of asset loss or degradation. Asset

custodians are commonly held to a fiduciary standard of care. A BBLLC approach

emphasizes a digital distributed trust model; BBLLC’s, however, may be

challenged with off-chain enforcement actions and physical custody operations

(e.g., physical asset audits). BBLLC custodians may require insurance to

protect asset owners in the event of asset losses/degradation.

If ownership of an asset, such as a

building, is split among thousands of people, there is little incentive for

owners to bear the costs associated with that asset, such as maintenance and

ensuring rent is collected [Deloitte 2018]. One can certainly imagine a smart

contract detecting that rent has not been credit to an account, but what then

can be done in terms of off-chain enforcement? While IoT blockchains can enable

significant cyberphysical functionality, typical landlord capabilities of

self-help and legal dispossessory actions would seem technically difficult or

socially problematic. Some classes of contracts requiring off-chain enforcement

actions may not be a good fit for complete implementation by dApp smart

contracts at this stage; and may still require human physical agents or other

legal entities for some actions.

Because the transaction of tokens is

completed with smart contracts, certain parts of the exchange process are

automated. For some classes of transactions, this automation can reduce the

administrative burden involved in buying and selling, with fewer intermediaries

needed, leading to not only faster deal execution, but also lower transaction

fees [Deloitte 2018]. Elimination of intermediaries sounds financially

efficient; eliminating all intermediaries, however, may not be wise for some

classes of assets. An intermediate entity may be useful as a liability shield

for remote owners. Consider a tokenized mobile asset (e.g., a drone or

terrestrial vehicle) owned and operated via a smart contract, which injures

another or their property; most remote owners would insist on some limited

liability entity or insurance. While smart contract operated vehicles may not

be computationally feasible in the short term, even immobile asset classes like

real estate can result in liabilities for the owner (e.g., premises slip and

fall). The point being that for some set

of physical asset classes, the existence of at least one intermediate entity

for the purpose of liability shielding may be desirable.

By tokenizing financial assets—especially private securities or typically illiquid assets—these tokens can be then be traded on a secondary market of the issuer’s choice, enabling greater portfolio diversification, and capital investment in otherwise illiquid assets. Tokenization could open up investment in assets to a much wider audience through reduced minimum investment amounts and periods. Tokens can be highly divisible, meaning investors can purchase tokens that represent incredibly small percentages of the underlying assets. If each order is cheaper and easier to process, it will open the way for a significant reduction of minimum investment amounts [Deloitte 2018]. Token markets to date have often been via exempt ICOs that are restricted to accredited investors, minimizing regulatory filings, etc. Investment minimums are unlikely a major driver for accredited investors, though enabling investment in diverse, but otherwise illiquid asset classes may be of interest for portfolio diversification. Enabling liquidity for mass market investors would require security token investments to meet the necessary higher regulatory standards for filings and disclosures to bring those investments to the larger public markets.

Smart contracts offer efficient process automation for trading and other transactions based on tokenized assets. While this can provide market efficiencies, not all asset classes are ready for tokenization without further consideration. Smart contracts may also need to take on additional behaviors to reflect the increased importance of their role in administering assets. Standardizing token formats and behaviors for different asset classes and business models should lead to improved interoperability, wider adoption, and more meaningful dialogs with regulators, investors and entrepreneurs.

References

[Alharby 2018] M. Alharby, et. al.,

“Blockchain-based smart contracts: A systematic mapping study of academic

research (2018).” Proc. Int’l Conf. on Cloud Computing, Big Data

and Blockchain. 2018.

[Bartoletti 2017] M. Bartoletti & L. Pompianu.

“An empirical analysis of smart contracts: platforms, applications, and

design patterns.” International conference on financial

cryptography and data security. Springer, Cham, 2017.

[Cai 2019] T.Cai, et al. “Analysis of Blockchain

System With Token-Based Bookkeeping Method.” IEEE Access 7

(2019): 50823-50832.

[Clack 2019] C. Clack, & C. McGonagle. “Smart

Derivatives Contracts: the ISDA Master Agreement and the automation of payments

and deliveries.” arXiv preprint arXiv:1904.01461 (2019).

[Fedosov 2018] A. Fedosov, et. al., “Sharing

physical objects using smart contracts.” Proceedings of the 20th

Int’l Conference on Human-Computer Interaction with Mobile Devices and Services

Adjunct. ACM, 2018.

[Hong 2019] S. Hong, et. al., “Design of

Extensible Non-Fungible Token Model in Hyperledger Fabric.” Proc.

of the 3rd Workshop on Scalable and Resilient Infrastructures for Distributed

Ledgers. ACM, 2019.

[Krishna 2004] P. Krishna, et.al., “An EREC framework

for e-contract modeling, enactment and monitoring.” Data &

Knowledge Engineering51.1 (2004): 31-58.

[Lo 2019] Y. Lo, et. al., “Assets on the

Blockchain: An Empirical Study of Tokenomics.” Available at SSRN

3309686 (2019).

[Migliorini 2019] S. Migliorini, et. al., “The

Rise of Enforceable Business Processes from the Hashes of Blockchain-Based

Smart Contracts.” Enterprise, Business-Process and Information

Systems Modeling. Springer, Cham, 2019. 130-138.

[Morrow 2019] M. Morrow, & M. Zarrebini.

“Blockchain and the Tokenization of the Individual: Societal

Implications.” Future Internet 11.10 (2019): 220.

[Mouloud 2019] K. Mouloud, “Blockchain in the Music

Industry: A Study of Token Based Music Platforms” S. Diss. Aalborg

University, 2019.

[Soumin 2018] S. Somin, et. al., “Network

analysis of erc20 tokens trading on ethereum blockchain.” International

Conference on Complex Systems. Springer, Cham, 2018.

[Victor 2019] F. Victor, & B. Lüders,

“Measuring Ethereum-based ERC20 token networks.” International

Conference on Financial Cryptography and Data Security. Springer, Cham,

2019.

Much of the excitement in recent blockchain literature has been concerned with the potential for “smart contracts” executing autonomously on a blockchain, while (immutably) preserving transaction records. The first use of the “smart contract” term is generally credited to Szabo [Szabo 1997], [Szabo 2002]. [Gisler 2000] proposed requirements for electronic contracts to support legal aspects. Automated execution of electronic contracts predates blockchains and Nakamoto’s Bitcoin paper [Nakamoto 2008]. Automated trading systems were being discussed in the early 1990’s (see e.g., [Domowitz 1990]). Enterprise Resource Planning systems were being extended to detect actual and imminent contractual violations in the early 2000’s (see e.g., [Xu 2003]). XML proposals were made for capturing electronic contracts [Krishna 2004]. [Grigg 2004]’s Ricardian contracts proposal added parameters and prose beyond the code. A markup language for facilitating translating contracts from a human-oriented form into an executable representation for monitoring was developed by [Governatori 2005]. The availability of the solidity programming language in Ethereum [Buterin 2014] created additional momentum with a significant uptick in smart contract related publications starting in 2014 [Macrinici 2018].

The “smart contract” term,

originally coined to refer to the general automation of legal contracts, seen a

resurgence of interest due to the advent of blockchain technology. Given the

variety of systems proposed and the complexity of the technologies underlying

smart contracts it is difficult to evaluate many claims concerning their actual

capabilities and real potential to change the commercial and legal landscape

[Mik 2017]. Generally, smart contracts are computer protocols that implement

the terms of a negotiated contract in a self-executing manner [Cieplak 2017]. Recently,

the term is popularly used to refer to low-level code scripts running on a

blockchain platform [Bartoletti 2017]. [van der Laan 2019] refers to smart

contracts as applications that are deployed and executed on a blockchain’s

decentralised infrastructure. [Rouhani 2019] considers the smart contract to be

a programmable transaction that can perform a sophisticated task, execute

automatically, and store on the blockchain. For [Di Angelo 2019a], smart

contracts on a blockchain are programs running in a distributed, transparent,

and trustless environment. Smart contracts for [Macrinici 2018], are

essentially containers of code that encode and mirror the real-world

contractual agreements in the cyber realm. Smart contracts are software

programs featuring both traditional applications and distributed data storage

on blockchains; acting as autonomous agents in critical decentralized

applications according to [Praitheeshan 2019]. While the possibilities are

endless, this does not help us decide whether a particular thing is or is not a

smart contract.

More formally, [ISO 2019] recently defined a smart contract as a computer program stored in a distributed ledger system wherein the outcome of any execution of the program is recorded on the distributed ledger; noting, however, that a smart contract might represent terms in a contract in law and create a legally enforceable obligation under the legislation of an applicable jurisdiction. Some assets manageable by smart contracts (e.g., bitcoin) have been deemed commodities for regulatory purposes. Cryptocurrencies as blockchain applications also fit within this definition of a smart contract [Geirgat 2018]. A regulator [CFTC 2018] issued guidance on smart contracts describing them as fundamentally a set of computer functions, but also noted that they may incorporate elements of a binding (i.e., legally enforceable) contract. The International Swaps and Derivatives Association (ISDA) defines [Clack 2019] a smart contract as an automatable and enforceable agreement; automatable by computer, although some parts may require human input and control; enforceable either by legal enforcement of rights and obligations or via tamper-proof execution of computer code. Blockchain technology provides a platform for the decentralized execution of smart contracts. The class of programs executing in a decentralized manner and storing results in a blockchain includes smart contracts; not all such blockchain decentralized applications (dapps), however, are required to have any association with a contract; nor are autonomous programs executing legal contracts required to be decentralized. For the purposes of most technology-focused discussions, it would be less confusing to refer to dapps rather than smart contracts unless the dapp is envisaged as fulfilling some specific contractual function.

As computer code, a smart contract

executes in the context of a particular virtual machine supported by a

particular blockchain. Smart contracts can invoke other smart contracts

executing in the same or other blockchains. Not all data sources for the smart

contract are natively found in the environment of a single blockchain. A smart

contract is an agreement that is automatically executed when certain conditions

are met [Fournier 2019]. “Oracles” provide a mechanism for off-chain data to be

made available for the smart contract executing in the blockchain. Many early

smart contracts have been focused on financial applications. Off-chain

financial data inputs to a smart contract might be prices of assets, or

confirmation of trades from other blockchains, e.g. in an exchange between

bitcoin and some other cryptocurrency. Hence, we can conclude that a smart

contract executing in one particular blockchain environment may have

input/output operations on its own blockchain or on an arbitrary number of

other blockchains.

A key feature of smart contacts is the autonomous algorithmic execution based on a mapping of certain detectable states of nature to corresponding contractual actions [Bakos 2019]. With the advent of IoT blockchains, a broad range of cyber-physical data from sensors can become an input to smart contracts. To release their potential, it is necessary to connect the contracts with the outside world, such that they can understand and use information from other infrastructures [Guarnizo 2019]. Beyond financial applications, blockchains are also being proposed to control devices in the physical world [Lee 2019]. This implies that blockchain smart contracts could be used to control not just digital assets, but also physical devices. A smart contract is not required by its definition to have physical I/O. hence smart contracts may have [0..n] inputs or outputs in the physical world.